Injured in Ontario? Get clear legal guidance today.

Our personal injury team can help with accident, disability, and injury claims. Contact us today for a free consultation.

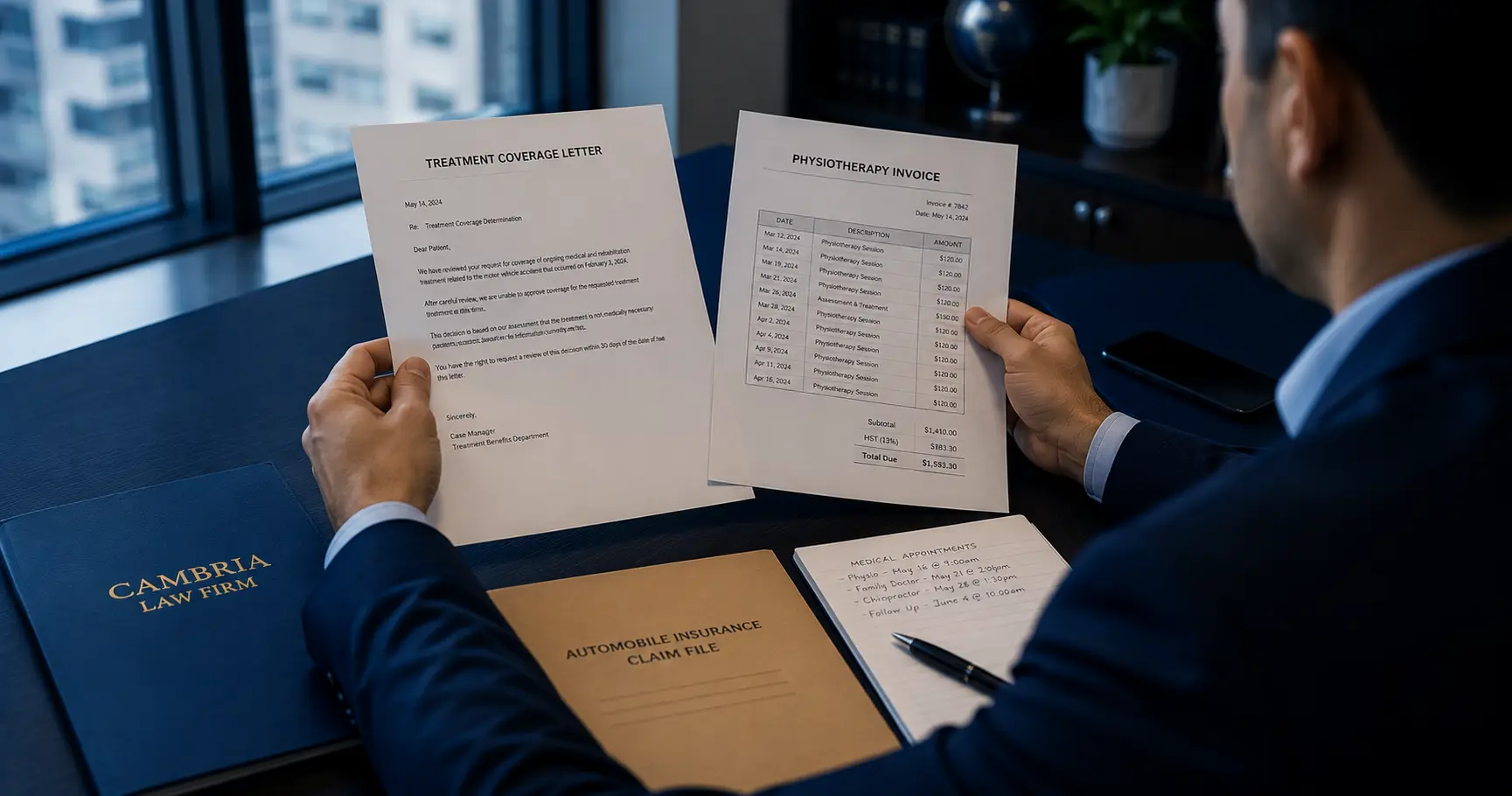

Being told that OHIP will not pay for accident-related treatment does not necessarily mean that no coverage is available.

OHIP may continue to cover insured physician and hospital services, while automobile accident benefits, WSIB, private health insurance, or another source may be responsible for rehabilitation, income replacement, attendant care, equipment, or other expenses. The first step is to identify exactly what was refused and which system applies.

After an accident, patients sometimes hear that “OHIP will not cover” a treatment, assessment, or rehabilitation service.

That statement can mean several different things. It may mean that the patient’s OHIP eligibility needs to be confirmed. It may mean that the particular service is not insured by OHIP. It may also mean that another benefit system—such as automobile accident benefits or WSIB—is expected to respond.

These are different problems with different solutions.

The most important first step is to obtain a clear explanation before paying a large bill, abandoning treatment, or assuming that no other coverage exists.

The phrase “OHIP denied my claim” is often imprecise. Patients do not usually submit a personal injury claim directly to OHIP in the same way they submit an insurance or WSIB claim.

The issue may instead be one of the following:

Keep copies of letters, invoices, treatment plans, estimates, and written explanations. A clear record will help determine whether the issue is administrative, contractual, or legal.

A motor vehicle or workplace accident does not automatically eliminate OHIP coverage.

Eligible insured physician and hospital services may continue to be covered through OHIP. However, many additional services commonly required after an injury are not universally insured by OHIP.

Depending on the circumstances, these may include:

The fact that a service is not funded by OHIP does not necessarily mean that the expense must remain unpaid. The appropriate source may depend on how the accident happened and which policies or statutory programs apply.

If the injury arose from a motor vehicle accident, the injured person may be entitled to Statutory Accident Benefits under Ontario’s automobile insurance system.

These benefits may apply to drivers, passengers, pedestrians, and cyclists. A claimant does not necessarily need to own a vehicle or hold an automobile insurance policy personally.

Depending on the policy, accident date, injuries, and coverage available, accident benefits may include:

Ontario’s statutory priority rules determine which insurer should receive the application. The appropriate insurer may be the claimant’s own insurer, another policy under which the claimant is insured, an insurer connected to an involved vehicle, or the Motor Vehicle Accident Claims Fund when no insurance responds.

An OCF-3 Disability Certificate may be required for certain benefit claims, but it is not necessarily required in every file. Other forms may also apply depending on the claimant’s employment, injuries, treatment plan, and requested benefits.

An accident should generally be reported to the insurer within seven days or as soon as reasonably practicable. The completed OCF-1 is generally returned within 30 days after the application package is received.

Late notice or late forms can lead to disputes and may affect entitlement. However, a delay does not automatically mean that every claim is permanently lost. The reason for the delay and the applicable rules must be reviewed.

If the accident happened at work or arose from employment, WSIB coverage may apply where the worker and employer fall within Ontario’s workplace insurance system.

Not every worker, employer, or industry is treated identically. Coverage should be confirmed rather than assumed.

Workers should not assume that an employer’s report alone fully protects the claim. WSIB generally requires a worker to claim benefits within six months of the accident or diagnosis, although extensions may be available in limited circumstances.

If WSIB denies the claim, the decision letter should be reviewed immediately because objection and appeal deadlines may apply.

Sometimes the treatment issue is not caused by the accident. The person’s health coverage information may be incomplete or their eligibility may need to be confirmed.

Possible issues include:

Ontario no longer imposes a general waiting period for OHIP coverage on people who are eligible. The issue is whether the person meets the current eligibility requirements and can provide the required documents.

Where health coverage eligibility intersects with immigration status, separate immigration advice may be appropriate. That issue should be reviewed independently from the personal injury claim.

It is inaccurate to assume that OHIP never funds physiotherapy after an accident.

Government-funded physiotherapy may be available to eligible patients, including:

Eligibility for a publicly funded program does not guarantee that every clinic, service, or treatment plan will qualify. Patients should confirm the current requirements directly with the clinic or provincial program.

Where publicly funded physiotherapy is unavailable, automobile accident benefits, WSIB, private insurance, or a civil claim may provide another potential source of payment.

Depending on the accident and the person’s policies, expenses may also be considered under:

Coverage coordination can be complicated. A provider may need pre-approval, a treatment plan, an insurer claim number, or proof that another plan has already responded.

Create one physical or digital folder containing:

After an important call, record the date, the person’s name, the department, what was discussed, and any reference number provided.

Before paying privately, ask the provider:

Where payment is necessary, keep the invoice, proof of payment, prescription or referral, and any document connecting the treatment to the accident.

Early legal advice is often about avoiding errors and protecting deadlines rather than immediately starting a lawsuit.

A personal injury lawyer may assist with:

How Cambria Law Firm Can Help

Many community-based physiotherapy services after a motor vehicle accident are pursued through automobile accident benefits rather than OHIP. However, government-funded physiotherapy may remain available to specified eligible groups, including certain younger and older patients and some people following hospitalization or surgery.

An accident should generally be reported to the insurer within seven days or as soon as reasonably practicable. The OCF-1 is generally returned within 30 days after the claimant receives the application package. A late application should be submitted with an explanation rather than abandoned.

The OCF-1 is the Application for Accident Benefits used to begin an Ontario automobile accident benefits claim. Additional forms may be required depending on the benefits sought.

They may. Ontario accident benefits can apply to pedestrians and cyclists injured in motor vehicle accidents. Statutory priority rules determine which insurer or fund receives the application.

Two refusals may reflect different issues, including an uninsured service, missing pre-approval, incomplete forms, a coordination-of-benefits dispute, or disagreement about whether the treatment is reasonable and necessary. Obtain both decisions in writing and review the reasons before assuming that no remedy exists.

The Motor Vehicle Accident Claims Fund is an Ontario fund of last resort that may respond where no automobile insurance is available, subject to statutory eligibility requirements and limitations.

A worker generally has six months from the accident or diagnosis to claim WSIB benefits. Shorter practical reporting timelines may apply to employers and healthcare providers, so workplace injuries should be reported promptly.

Not necessarily. Another insurer or statutory benefit system may apply.

Incorrect. Passengers, pedestrians, and cyclists may qualify for automobile accident benefits.

Not always. Eligibility and card validation should be confirmed directly with ServiceOntario and the healthcare provider.

Insurers provide claims information, but claimants should independently understand the forms, benefits, deadlines, and evidence relevant to their circumstances.

Related services:

Our personal injury team can help with accident, disability, and injury claims. Contact us today for a free consultation.