Injured in Ontario? Get clear legal guidance today.

Our personal injury team can help with accident, disability, and injury claims. Contact us today for a free consultation.

In Ontario, a long-term disability claim and a personal injury claim can often run at the same time.

The challenge is coordinating deadlines, medical records, offsets, subrogation, and settlement strategy so one file does not accidentally damage the other.

If you are an Ontario employee on a group long-term disability (LTD) policy and you were injured because someone else was at fault, it is normal to feel stuck.

You may be dealing with an LTD application or an LTD denial, while also wondering if you should start a personal injury claim for the same incident. For example: a slip and fall, an unsafe property, a negligent driver in a non-SABS situation, or another preventable injury.

The core confusion is this: LTD benefits come from a private insurance contract through your workplace. A personal injury claim is a civil claim for compensation against an at-fault party, usually their liability insurer. One does not automatically cancel the other.

What usually creates overlap problems is not eligibility. It is these issues:

Yes. You can often have both an LTD claim and a personal injury claim at the same time because they are separate systems with different legal foundations and different payors.

LTD is contractual. Your right to LTD benefits comes from the terms of your group policy. If you meet the policy definition of disability and satisfy the proof requirements, the insurer may have to pay monthly benefits.

A personal injury claim is civil litigation. Your right to compensation comes from proving that another party was negligent or otherwise legally responsible and that their actions caused your losses. The defendant is usually the at-fault person or organization, and the money typically comes from their liability insurer.

In such cases, it may be useful to consult with a long-term disability lawyer who can help navigate the complexities of your LTD application or denial. If you are also considering a personal injury claim due to someone else’s negligence, advice from an Ontario personal injury lawyer can help you understand how the two files interact.

You do not usually have to choose one or the other at the start.

But “separate” does not mean there is no financial interaction later. Most group LTD policies have clauses that can affect what you keep if you later recover money in a personal injury settlement or judgment. That is where subrogation and coordination language matters.

LTD does not protect your lawsuit deadline.

You can be receiving LTD every month and still lose your right to sue if you miss Ontario’s limitation deadline for starting a lawsuit.

Ontario’s basic limitation period for most personal injury lawsuits is two years. In many cases, that two-year clock starts running from the accident date or from when you first knew, or should have known, that you had a legal claim against an identifiable party.

If you wait “until you feel better” or “until LTD is sorted out,” you can miss the deadline and permanently lose your ability to sue.

The limitation analysis is fact-specific, but these are common trigger points to discuss early:

If you are dealing with a slip and fall incident, it is important to seek legal advice promptly to preserve your rights.

If you are considering settlement with insurance companies after an accident, it is also important to understand why accepting the first insurance offer may not be in your best interest.

One reason these files can coexist is that they do not pay for the same things in the same way.

Group LTD is primarily income replacement.

Most policies pay a percentage of pre-disability earnings, subject to:

LTD is not designed to fully compensate you for everything you lost. It is designed to pay a contractual monthly benefit if you meet the policy test.

A personal injury claim is intended to pursue full compensation under Ontario civil law, depending on the facts and the type of defendant.

Common heads of damages can include:

The categories and available damages depend on the type of incident and the legal framework that applies. The key point is this: a personal injury claim is not just “more disability benefits.” It may address long-term costs and losses LTD does not cover.

In Ontario, LTD is private insurance. It is governed by the policy contract and the provincial insurance framework, including Ontario’s Insurance Act. It is not a government program.

That matters because the insurer’s rights and your obligations are driven by the policy wording and the documents you sign.

LTD forms often include broad authorizations allowing the insurer access to medical records and other information.

That information can later be used to challenge:

This does not mean you should withhold legitimate medical information. It means you should understand what you are signing and keep your reporting accurate and consistent.

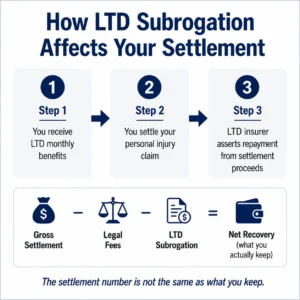

Subrogation is the issue that surprises most people at settlement time.

Subrogation is a policy term that may allow your LTD insurer to recover amounts it paid to you if you later recover money from an at-fault party for the same loss.

In practice, an LTD insurer may assert a repayment claim against your settlement proceeds once your personal injury claim resolves. You might hear this described as a lien, reimbursement claim, or subrogation claim.

Many personal injury cases settle months or years after the injury. By that point, the LTD insurer may have paid significant benefits.

When the personal injury settlement is being negotiated or finalized, the LTD insurer may require that its repayment position be addressed before funds are released.

The settlement number is not the same as what you keep.

If subrogation applies, repayment can reduce your net recovery. The impact depends on the policy wording, the amounts paid, and how the settlement is structured and documented.

For example, if you suffered a catastrophic injury or a whiplash soft tissue injury, these factors can significantly influence your settlement amount and any related subrogation issue.

Subrogation rights are typically driven by:

Because the policy is a contract, details matter. Two policies can look similar but produce very different repayment outcomes.

Settlement discussions often focus on a single number. That number is usually the gross amount.

What matters to you is the net amount.

A typical personal injury settlement can be reduced by:

A defendant’s offer might look reasonable until you subtract what must be repaid.

If subrogation exposure is significant, the negotiation focus often shifts to:

Keep a simple benefits ledger:

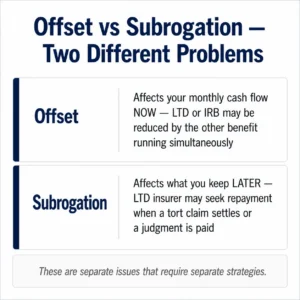

Offsets are different from subrogation.

Subrogation usually matters when you recover money from an at-fault party later. Offsets affect monthly cash flow now.

Under the SABS, income replacement benefits can be reduced by other income replacement sources such as LTD or WSIB benefits, depending on the circumstances and applicable coordination rules.

You may not receive full LTD and full IRB at the same time. One benefit may be deducted from the other.

This creates cash-flow stress quickly, especially when you are off work and still paying rent or a mortgage. It also creates paperwork problems if the LTD insurer, the accident benefits insurer, and your doctors are not aligned on restrictions and prognosis.

A personal injury settlement does not automatically terminate LTD benefits.

Your LTD entitlement depends on the policy definition of disability and the proof you provide. If you remain disabled under the policy test, benefits may continue.

What can change after settlement is the insurer’s financial position and scrutiny.

Do not rely on informal or artificial allocations meant to avoid subrogation.

Any allocation in settlement documentation should be defensible and consistent with the medical, vocational, and financial evidence. If the paperwork does not match the reality of the claim, it can create problems with the LTD insurer and can also complicate the settlement itself.

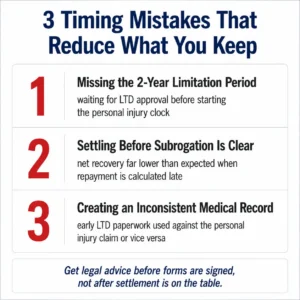

These processes move on different timelines, but they share evidence. That is why timing mistakes are expensive.

Do not wait for LTD approval before investigating and starting the personal injury claim. The two-year clock keeps running even if your LTD file is active.

If you settle without knowing the LTD insurer’s repayment position, you can end up with a net recovery that is far lower than expected. In some cases, the repayment issue becomes a settlement blocker late in the process.

Early LTD paperwork can create a narrative that later gets used against you in the personal injury case, or the reverse.

Common examples include:

Early legal advice is not only about suing. It is often about avoiding contradictions, missed deadlines, and preventable repayment surprises.

Many LTD packages include authorizations and requests that can be broader than people realize.

A review can help you understand:

If you are asked to give a recorded statement or attend an insurer interview, preparation matters. Inconsistent details are commonly used later to challenge credibility, causation, and functional impairment.

Before mediation or settlement, you want a clear picture of:

This article focuses on overlap, but an LTD denial can create financial pressure that affects settlement decisions in the personal injury case. Coordinating strategy early can avoid being forced into a rushed outcome.

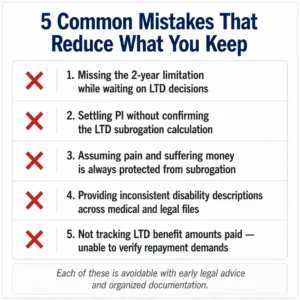

People often assume that because they are “in the system” with LTD, they are protected. They are not.

If there is a potentially liable party, the limitation period needs to be reviewed early and diarized.

If you settle first and ask questions later, you may learn that the net amount is not what you expected.

Confirm the LTD insurer’s position and get updated paid-to-date totals as the case progresses.

Some people believe that “pain and suffering is mine and cannot be touched.” That is not a safe assumption.

Whether subrogation reaches a settlement depends on the policy wording and what the settlement compensates. Confirm before you rely on general rules or internet advice.

Inconsistency is one of the fastest ways to damage both files.

Be accurate and consistent when describing:

Do not exaggerate. Do not minimize. Both approaches create problems.

If you do not have a ledger, it becomes harder to verify repayment demands quickly. That increases stress at mediation and can delay settlement closing.

If you are receiving or applying for LTD and you may also have a personal injury claim against an at-fault party, the goal is to coordinate the files early so you understand deadlines and likely repayment issues.

A focused review can address:

Cambria Law Firm, based in Mississauga, serves the Greater Toronto Area. Personal injury services are provided by Nav Aujla, Barrister and Solicitor, LSO #74895I. We handle personal injury claims across Mississauga and the GTA, including slip-and-fall injuries and catastrophic injuries.

To make the consultation efficient, gather:

Related reading:

Yes, you can have both an LTD claim and a personal injury claim at the same time because they are separate systems with different legal foundations and payors. LTD benefits come from your workplace’s group insurance policy, while personal injury claims are civil lawsuits against an at-fault party.

An LTD claim is contractual, based on your group insurance policy through your employer, providing monthly benefits if you meet the disability definition. A personal injury claim is civil litigation seeking compensation from someone who was legally responsible for your injury, usually their liability insurer.

Receiving LTD benefits does not automatically cancel your right to file a personal injury lawsuit. However, most group LTD policies include clauses like subrogation and coordination of benefits that may affect how much money you keep if you later recover funds from a personal injury settlement or judgment.

In Ontario, the basic limitation period for most personal injury lawsuits is two years from the date of the accident or when you first knew, or should have known, about your legal claim. This two-year deadline applies regardless of whether you are receiving LTD benefits, so it is crucial not to miss it.

You should diarize the two-year limitation deadline with early reminders, preserve all evidence such as photos and incident reports, identify witnesses and keep their contact information, and maintain detailed treatment and work-absence records. Prompt action can preserve your rights and strengthen both claims.

Navigating LTD applications or denials alongside potential personal injury claims can be complex due to overlapping issues like limitation periods, subrogation, and benefit coordination. Legal advice can help you understand your rights, meet deadlines, and avoid preventable mistakes that reduce your recovery.

Our personal injury team can help with accident, disability, and injury claims. Contact us today for a free consultation.