Injured in Ontario? Get clear legal guidance today.

Our personal injury team can help with accident, disability, and injury claims. Contact us today for a free consultation.

A recorded statement is not just a routine insurance call. It can become evidence used against you later.

Before giving a recorded statement after a car accident or slip and fall in Ontario, understand which answers can damage your claim and when to pause for legal advice.

After a car accident or slip and fall in Ontario, one of the first calls you receive from an insurer will often include a request for a “quick recorded statement.” It sounds routine. It is not.

A recorded statement is one of the earliest opportunities an insurer has to lock you into a version of events — often before your injuries have fully declared themselves, before you have reviewed any documents, and before you have had a chance to understand what your claim actually involves. Anything said on that recording can be replayed later to argue you were not injured, that you were at fault, or that you are not entitled to the benefits or compensation you are seeking.

This article covers the nine statements that most commonly damage Ontario injury claims, and what to say instead.

A recorded statement is a formal question-and-answer session with an insurance representative, recorded by audio or video, typically described to claimants as routine or administrative. The insurer can use it to establish your early account of events, compare your answers against medical records and other statements as the claim develops, identify inconsistencies, and build arguments for reducing fault, limiting coverage, or lowering the value of your claim.

The first day or two after an accident is among the worst times to make permanent, replayable statements. You may be in pain, on medication, operating on little sleep, or simply trying to manage the immediate disruption to your life. That is exactly when insurers prefer to call.

This is the most common damaging statement and the most understandable one. People say it instinctively — in shock, not wanting to escalate, trying to end the call. But “I’m fine” becomes part of a permanent record that insurers treat like a medical assessment.

Soft tissue injuries routinely worsen after the initial adrenaline subsides. Pain that appears manageable in the first hours can become significant by day two or three. If you later report neck pain, headaches, dizziness, sleep disruption, or numbness, the insurer will point to your early recorded statement and argue you reported no injury.

What to say instead: “I’m still sore and still being assessed. I don’t have a full picture of my injuries yet.” That is accurate, it is not dramatic, and it does not close any doors.

Do not admit fault in a recorded statement, regardless of how you feel about the accident in the immediate aftermath. Fault is a legal conclusion, not a personal feeling — and it is not yours alone to determine.

In Ontario, fault analysis involves road conditions, visibility, speed, signage, right of way, lane positioning, timing, and witness evidence. You likely do not have all of that information when the insurer calls. Saying “it was my fault” because you felt guilty, or because you did not react in time, or because you were confused about what happened, may not accurately reflect the legal reality once all the facts are established.

What to say instead: Stick to observable facts. What you saw, what you did, what happened. Do not label it.

Both of these statements can be used to argue you were not paying attention — that you failed to observe a hazard you should have seen. “I didn’t see them” can be framed as inattention. “They came out of nowhere” can be framed as you were surprised because you were not watching your surroundings properly.

Accidents happen quickly and memory is frequently imperfect immediately after a collision. If you are genuinely uncertain about what you saw or when, say that.

What to say instead: “It happened very quickly. I’m not fully certain about what I observed and I don’t want to speculate.”

You do not know yet. “Minor” is exactly the language insurers want in a recorded statement — it is used to support Minor Injury Guideline classification, which caps your medical and rehabilitation benefits at $3,500 and limits the treatment funding available to you.

Pain that feels manageable in the immediate hours after an accident can become weeks or months of physiotherapy. Describe what you are actually experiencing rather than labelling its severity.

What to say instead: “I have pain when I turn my neck.” “I’ve been having headaches.” “I’m stiff in the morning and I’m still being assessed.” Factual, specific, and not a self-diagnosis.

If you later see a doctor, physiotherapist, or other healthcare provider, the insurer will use this statement to argue you are exaggerating later injuries or that something else caused them. It also provides an opening to argue that the injuries were not serious enough to require care.

If you have not yet seen a medical professional, say that. If you are planning to or have been advised to, say that. What you know at the time of the call is that you have not yet been fully assessed — that is the accurate statement. How your medical documentation subsequently develops shapes the entire claim. Our post on how doctor notes affect your injury claim covers why that early record matters so much.

Genuine memory gaps after an accident are real and common. But defaulting to “I can’t remember” as a way of managing pressure or avoiding difficult questions creates a credibility problem later.

Slow down. If a detail is genuinely uncertain, the right answer is a precise one: “I’m not sure about the exact time,” “I don’t recall that specific detail,” “I would need to check,” or “I don’t want to guess.” That last response is particularly important — guessing creates contradictions that become ammunition later.

People sometimes volunteer information that was never asked — admitting they were speeding, glancing at their phone, or distracted — either out of nervousness, a desire to be honest, or because they feel guilty. A recorded statement is not a confession. It is evidence.

If you are asked a direct question, answer it truthfully and narrowly. Do not expand beyond what was asked. Do not narrate your entire day. If you do not fully understand the question, ask them to repeat or clarify it before answering.

Many people want to establish that the accident caused their injury, so they overstate how free of prior issues they were. But if medical records later show chiropractic treatment, an old sports injury, prior back pain, previous anxiety, or a past concussion, the insurer will use your statement to allege dishonesty — even if the prior issue was unrelated or fully resolved.

Prior history does not automatically harm an Ontario injury claim. An accident that aggravates or accelerates a pre-existing condition is still a compensable injury. But an inconsistent statement about that history is genuinely damaging.

What to say instead: “I’ve had some prior issues with [area] but they were stable before this accident.” Accurate, not defensive, and not a gift to the insurer.

The moment you agree to be recorded, the statement begins — and whatever state you are in at that moment becomes the permanent record. If you are in pain, on medication, at work, in a noisy environment, emotionally overwhelmed, or simply have not yet had time to review the accident report or understand what coverage you have, that is not the moment to agree to a recorded statement.

You are permitted to say you are not ready and to request time. “I’m not in a position to provide a recorded statement right now. I’ll respond when I’m able.” Consider getting legal advice before agreeing, particularly if the circumstances involve fault disputes, significant injuries, or questions about alcohol, phone use, or speed. Insurers use all available evidence — including recorded statements — to build their position, and an early statement given under pressure is one of the most avoidable errors in a claim.

If alcohol is in any way involved in the accident, do not characterize or summarize it casually. The consequences in an Ontario claim context — both for coverage and for fault — can be significant. This is a situation where legal advice before any further statements is strongly advisable.

Even if you are having a relatively good day, healing from an injury is rarely linear. If you state you are fully recovered and symptoms later return or worsen, the insurer will frame it as inconsistency. Describe your current functional status accurately rather than optimistically. “I’m having some better days but symptoms are still present” is more accurate and more defensible than “I’m back to normal.”

Some forms that insurers send are routine. Some authorization forms are very broad and can permit access to extensive medical records well beyond what is relevant to your claim. Read everything before signing, and ask for time to review if needed.

Before answering recorded questions, slow the process down.

Early statements are valuable to insurers because they happen before you have received a medical diagnosis, before you have reviewed the accident report or gathered witness information, before you understand what coverage you have or what your claim involves, and when stress and adrenaline make precise, careful answers less likely. This is not personal — it is strategic. Understanding that changes how you approach the call. Our post on why not to accept the first insurance offer covers related insurer pressure tactics at later stages of a claim.

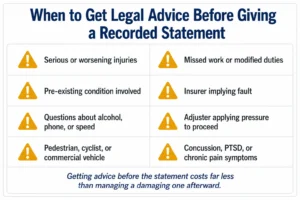

The following situations warrant legal advice before you agree to any recorded statement:

Ontario injury claims can escalate quickly once accident benefits, tort claims, and limitation periods are in play simultaneously. A recorded statement given before you understand the full picture of your claim is one of the most common and most avoidable errors.

Related reading:

There is a general obligation under Ontario insurance policies to cooperate with your insurer’s investigation, which can include providing information about the accident. However, you are not obligated to provide a recorded statement immediately on demand, particularly under conditions that are not conducive to careful and accurate answers. You can request time to prepare and can seek legal advice before proceeding. If your insurer is suggesting immediate recorded statement cooperation is mandatory on their schedule, speaking with a personal injury lawyer before complying is advisable.

Not necessarily. Many people make casual statements at the scene or in early calls that do not accurately reflect the full extent of their injuries. This is a known pattern and courts and tribunals are aware that adrenaline and shock affect early self-assessment. The more important issue is what you do from that point forward: seek medical assessment promptly, report all symptoms accurately to every healthcare provider, and ensure your medical record reflects your actual condition. A single early statement is one piece of evidence, not the whole claim.

You can make this request. Some insurers will accommodate written statements, particularly for accident benefits purposes. Whether a written versus recorded format is more advantageous depends on your specific situation. Getting legal advice about the format and content of your statement before providing it is the most protected approach.

Do not panic. A recorded statement is one piece of evidence in a claim that will be decided based on the totality of the record — including medical documentation, witness accounts, expert opinions, and your overall credibility over time. Consistent, accurate medical reporting going forward is the most effective way to address an early statement that does not reflect the full picture. Speak with a personal injury lawyer about how the statement may be addressed in the context of your specific claim.

Yes. Inconsistencies between a recorded statement and subsequent medical reporting, or statements that suggest your injuries were minor or resolved, are regularly cited by insurers when terminating or reducing accident benefits. This is one of the primary reasons early recorded statements carry significant risk — they can affect not just a tort claim but also your access to treatment funding and income replacement under the SABS.

You are entitled to have legal representation assist you in preparing for and, in some contexts, participating in a recorded statement. At minimum, speaking with a personal injury lawyer before giving a recorded statement in any situation involving significant injuries, disputed fault, or questions about alcohol or phone use is strongly advisable. The time spent on that preparation is significantly less costly than managing the consequences of a damaging early statement.

Our personal injury team can help with accident, disability, and injury claims. Contact us today for a free consultation.