Injured in Ontario? Get clear legal guidance today.

Our personal injury team can help with accident, disability, and injury claims. Contact us today for a free consultation.

If your insurer places you in Ontario’s Minor Injury Guideline, your medical and rehabilitation treatment funding is capped at $3,500.

Challenging a MIG classification requires medical evidence, consistent documentation, and a clear explanation of why your injuries should not be treated as minor.

If you were injured in a car accident in Ontario and an insurer has placed you in something called the Minor Injury Guideline, you are about to encounter one of the most consequential — and frequently disputed — classifications in the accident benefits system. Being in the MIG limits your treatment funding to a fixed cap. Getting out of it requires medical evidence, not phone calls to an adjuster.

This article explains what the MIG is, why insurers apply it aggressively, and what the recognized legal routes out of it actually look like.

The Minor Injury Guideline is a regulatory framework within Ontario’s Statutory Accident Benefits Schedule (SABS) — the accident benefits system that applies to all motor vehicle accidents in Ontario, regardless of fault. Understanding the broader 2026 SABS accident benefits framework is useful context before examining the MIG specifically.

The MIG creates a streamlined treatment pathway for injuries classified as “minor” and sets a hard cap on how much medical and rehabilitation funding the insurer must pay within that classification.

The difference between MIG and non-MIG classification is significant.

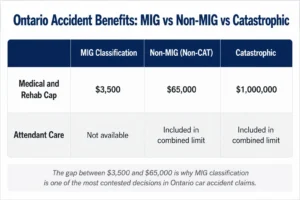

A MIG classification limits medical and rehabilitation funding to $3,500. A non-catastrophic claim outside the MIG may allow access to up to $65,000 in combined medical, rehabilitation, and attendant care benefits.

If your insurer places you in the MIG, your medical and rehabilitation benefits are capped at $3,500 total. The structure within that cap matters: an initial $2,200 of treatment can begin without prior insurer approval within the first 12 weeks, with any treatment plan beyond that requiring insurer approval up to the $3,500 ceiling.

That $3,500 has to cover physiotherapy, chiropractic treatment, massage therapy, rehabilitation exercises, diagnostic assessments, and anything else you need within the MIG framework. It runs out quickly for anyone with an injury requiring sustained or coordinated care.

For context: if your injuries are classified as non-catastrophic but outside the MIG, your combined medical, rehabilitation, and attendant care benefits rise to $65,000. For catastrophic injuries, the limit is $1,000,000. The gap between $3,500 and $65,000 is the reason MIG classification is so heavily contested.

The SABS defines a minor injury as one or more of the following: a sprain, strain, whiplash associated disorder (WAD), contusion, abrasion, laceration, or subluxation, including any clinically associated sequelae — meaning symptoms that are clinically connected to those injuries, such as headaches related to a whiplash strain.

Notice what is not on that list: fractures, concussions, disc herniations, significant ligament or tendon tears, nerve injuries, psychological injuries such as PTSD or anxiety disorder, and chronic pain syndromes. These injuries should, by the SABS definition, fall outside the MIG. The problem is that insurers frequently apply the MIG classification based on the initial clinical presentation — often a complaint of neck or back strain — before the full picture has developed.

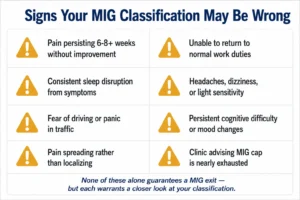

A significant number of people who begin with what looks like a strain find that their injury does not resolve within the 12-week MIG framework. It becomes chronic. It develops neurological signs. It triggers anxiety, sleep disruption, and dizziness. It interacts with a pre-existing condition in ways that make MIG-level treatment insufficient. That is where the MIG classification begins to break down and where a challenge becomes appropriate.

The financial incentive is straightforward. A MIG classification limits the insurer’s treatment cost exposure to $3,500. A non-MIG classification opens up to $65,000 in potential benefits. For borderline presentations — where the initial diagnosis is “sprain/strain” but the injury may be more complex — insurers have a strong financial motivation to maintain the MIG classification for as long as possible.

This is why early and detailed medical documentation matters so much. An insurer maintaining MIG classification based on a thin initial file is a different situation from an insurer maintaining MIG classification against a well-documented, consistent medical record showing functional impairment beyond what minor injuries produce. See our guide on how doctor notes affect your injury claim for the documentation practices that matter most in this context.

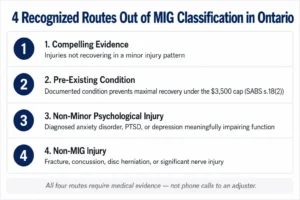

This is the broadest MIG exit route and comes into play when your injuries, though initially presenting as soft tissue, demonstrate a pattern that does not match a minor injury recovery trajectory. Examples include symptoms persisting significantly beyond the expected 12-week recovery window, a pattern of deterioration rather than improvement, significant functional impairment affecting work, caregiving, or daily activities, medical findings pointing to something beyond a simple strain, and psychological symptoms of substance.

What “compelling evidence” looks like in practice: consistent clinical notes from all treating providers, a clear and coherent symptom history from the date of the accident, documented functional restrictions (what you cannot do now that you could do before the accident), specialist referrals where appropriate, and diagnostic imaging where relevant. A thin file allows an insurer to maintain the MIG classification. A detailed, consistent file makes that position much harder to hold.

Under section 18(2) of the SABS, a person can be removed from the MIG if they have a documented pre-existing medical condition that will prevent them from achieving maximal recovery within the $3,500 cap. This is a well-established and evidence-heavy basis for a MIG exit.

Examples of pre-existing conditions that can support this argument include prior injuries to the same area of the body, arthritis or degenerative disc disease that was asymptomatic before the accident but was aggravated by it, chronic pain history, prior concussions, mental health history such as anxiety or depression that the accident worsened, and conditions like fibromyalgia that affect pain processing and recovery.

Two things are required: medical records from before the accident demonstrating the pre-existing condition existed, and evidence — typically from a treating physician or regulated health professional — explaining specifically why that condition means the MIG treatment cap is insufficient for recovery. A casual reference to prior pain is not enough. The connection between the condition and an inadequate recovery under MIG constraints needs to be made explicitly in the clinical record.

Psychological injuries that are not minor and not simply a secondary consequence of a physical minor injury can take a claim outside the MIG. After a collision, many people develop driving anxiety or avoidance, panic symptoms, nightmares, flashbacks, hypervigilance, mood changes, depression, or cognitive symptoms connected to trauma and sleep disruption.

When those symptoms meet clinical criteria for a recognized psychological condition — an anxiety disorder, major depressive disorder, PTSD — and they meaningfully impair daily functioning, the claim may fall outside MIG. The distinction between “feeling stressed after a crash” (which an insurer will treat as minor) and a properly diagnosed psychological injury (which an insurer must take more seriously) comes down almost entirely to documentation and diagnosis. Getting a proper psychological assessment early, not months into the claim, is what creates this MIG exit opportunity.

Some injuries are not minor by definition: fractures, dislocations, significant tendon or ligament tears, nerve injuries, moderate to severe concussions, and disc herniations. When these injuries are present, the MIG should not apply.

The practical problem is that these injuries are sometimes missed in initial emergency assessments or not diagnosed until weeks later. Whiplash sometimes masks concurrent neurological injury. Concussions are routinely underdiagnosed in emergency settings when CT imaging is normal — a normal CT does not rule out a concussion, and the Licence Appeal Tribunal (LAT) has consistently held that a credibly diagnosed concussion removes a claimant from the MIG.

Treatment delays give insurers an argument that the injury was not serious or that something other than the accident caused your symptoms. Even if you instinctively want to manage independently, getting assessed and beginning a clinical record early creates the baseline that everything else depends on.

Many people underreport how they are actually doing — either out of habit, out of wanting to appear capable, or because they do not realize how significantly the injury is affecting them until weeks later. If you have pain, stiffness, cognitive symptoms, sleep disruption, or anxiety connected to the accident, report all of it accurately at every clinical visit. The early chart entries are the hardest to change and the most heavily relied upon. See our post on how insurers use surveillance in injury claims for related context on why accurate and consistent reporting matters throughout the claim.

MIG exits require active steps — proper forms, medical reports that specifically address the MIG criteria, and often disputes through the formal process. The insurer has no obligation to reclassify you without documentation supporting it.

Ontario accident benefits claims are administered through a structured form system. The MIG issue typically surfaces around treatment plans. Relevant forms include:

If an OCF-18 seeking non-MIG funding is denied and the denial is based on MIG classification, the dispute resolution process through the Licence Appeal Tribunal (LAT) is the formal mechanism for challenging that decision. The LAT has developed a substantial body of decisions on MIG exits, and the evidentiary bar is evidence-based — not argument-based.

If your insurer denies benefits based on MIG classification and you believe that classification is wrong, our post on what to do when an insurance claim is denied in Ontario covers the dispute process in more detail.

These patterns do not automatically establish a MIG exit, but they should be taken seriously:

A consistent symptom timeline from the accident to the present — no unexplained gaps, no significant contradictions, early reporting of all symptoms — is the foundation. Functional impact documented throughout the clinical record carries more weight than pain ratings alone: what you cannot do now that you did before, specific work, caregiving, and daily activity restrictions, and the connection between those restrictions and the accident injury. How your claim affects pain and suffering valuation is also directly shaped by the quality of this functional documentation.

Diagnoses that evolve appropriately as the injury picture becomes clearer — from initial strain presentation to chronic pain syndrome, cervicogenic headaches, concussion with vestibular involvement, radiculopathy, or psychological injury — are more supportive of a MIG exit than a chart that reads identically at every visit with no clinical evolution.

Not always. Some people successfully move out of MIG with strong medical support from a clinic experienced in the accident benefits system. But if denials are recurring, if benefits are being cut despite documented clinical need, if insurer examinations are being used to maintain the MIG classification against your treating providers’ opinions, or if the injury is clearly non-minor and the insurer is not moving, legal advice becomes important.

Ontario’s two-year limitation period also applies to accident benefits disputes. The time to seek legal advice is before that window closes — not after.

Related reading:

Being placed in the Minor Injury Guideline means your insurer has classified your injuries as minor under the SABS definition, which caps your medical and rehabilitation benefits at $3,500 total. The initial $2,200 does not require prior insurer approval, but any treatment plan beyond that amount requires approval up to the $3,500 ceiling. Being in the MIG does not automatically limit other accident benefits such as income replacement, but it restricts the medical and rehabilitation funding available to you.

Under the MIG, medical and rehabilitation benefits are capped at $3,500. Outside the MIG, non-catastrophic injuries are eligible for up to $65,000 in combined medical, rehabilitation, and attendant care benefits. For catastrophic injuries, the combined limit is $1,000,000. The classification decision — MIG or non-MIG — is one of the most consequential determinations in an Ontario car accident claim.

No. Normal imaging does not mean a minor injury classification is correct. Concussions, soft tissue injuries, nerve irritation, and psychological injuries frequently produce normal imaging results. The MIG exit analysis is based on the clinical presentation, symptom history, functional impact, and medical opinions from treating professionals — not imaging results alone. The Licence Appeal Tribunal has consistently recognized that a credibly diagnosed concussion removes a claimant from the MIG even when imaging is normal.

Potentially yes. Under section 18(2) of the SABS, a documented pre-existing condition that will prevent you from achieving maximal recovery within the MIG cap is a recognized basis for removal from the MIG. You need pre-accident medical records establishing the condition existed and medical opinion explaining specifically why the condition prevents adequate recovery within the MIG framework. The pre-existing condition alone is not sufficient — the connection to an inadequate recovery must be explicitly established.

When the non-minor injury is clear from the outset — a fracture, a diagnosed concussion — the process can be relatively direct. In cases involving chronic soft tissue injury, persistent concussion symptoms, or psychological injuries, the MIG dispute often arises weeks or months into the claim when it becomes apparent that recovery is not following the expected minor injury trajectory. Acting earlier — when symptoms are not resolving — rather than waiting until the MIG cap is exhausted is significantly more advantageous.

Not in every case. Some MIG exits are resolved through proper medical documentation and a clinic experienced in the accident benefits system. Legal representation becomes more important when the insurer is using their own examination process to maintain MIG classification against your treating providers’ opinions, when benefits are being reduced or denied despite documented clinical need, or when the LAT dispute process is the next step. Getting legal advice early — before the dispute becomes entrenched — is generally more effective than seeking it after benefits have been denied repeatedly.

Our personal injury team can help with accident, disability, and injury claims. Contact us today for a free consultation.